Subject to the Articles, the directors of a corporation may declare and a corporation may pay a stock dividend by issuing fully paid shares of the corporation or options or rights to acquire fully paid shares of the corporation.

All shareholders of a corporation own shares. When a dividend is declared upon a class of shares of a corporation all shareholders that hold shares of that class are entitled to receive the dividend equally in proportion to the number of shares they own.

To understand how these dividends are declared, consider the following scenario. The directors of the Corporation approve a stock dividend on the issued common shares of a company on the basis of 10 common shares for every issued and outstanding share owned. The corporation has the following shareholders:

John Doe (holding 10 common shares)

Jim Holding Company Limited (holding 20 common shares)

If a stock dividend is declared on the issued shares of a corporation providing for ten:one ratio, after the stock dividend is issued the additional number of shares each shareholder will own is:

John Doe (10 x 10) – 100 common shares

Jim Holding Company Limited (20 x 10) = 200 common shares

The total number of shares owned by each shareholder including the original number of shares held and the additional shares allotted pursuant to the stock dividend are:

John Doe – 110 common shares

Jim Holding Company Limited – 220 common shares

Subsequent to the approval of a stock dividend each of the shareholders having a right to the stock dividend shall receive a share certificate for the additional shares they received.

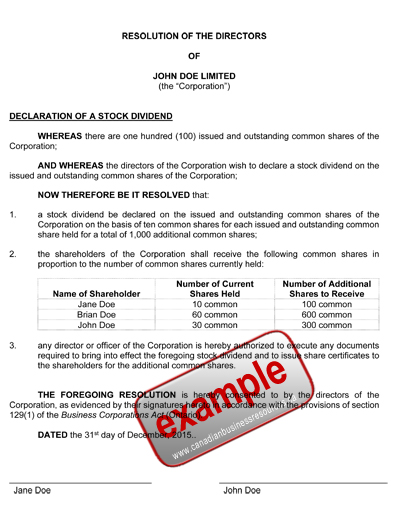

Below is an example of a directors resolution approving a stock dividend:

Buy Dividend Resolutions

If you wish to make things easy refer to this link for a number of templates that can be purchased relating to Approving Dividends Templates.

For more information about dividends refer to:

Capital Dividend Upon Redemption